For many students, bank reconciliations are a difficult topic because most people don’t do them anymore. Twenty years ago, before debit cards and online banking, there was only one way to keep track of how much money you had in the bank: keep a checkbook and reconcile it. Show

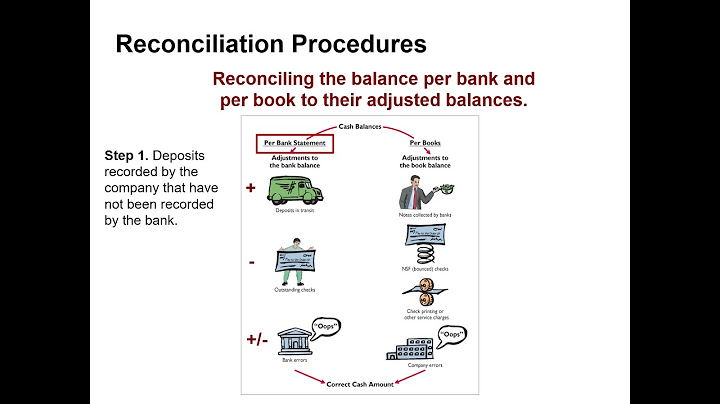

Clearly, online banking has not made us better at managing our bank accounts. In 2012, U.S. consumers paid $32 billion in overdraft fees. That’s approximately $135 per adult in the United States! Maybe we should consider going back to writing down all our transactions and balancing our checkbooks! What is a bank reconciliation?A bank reconciliation is a monthly process by which we match up the activity on the bank statement to ensure that everything has been recorded in the company’s or individual’s books. As we all engage in more automatic and electronic transactions, this is a critically important step to ensure that the cash balance is correct. There are two parts to a bank reconciliation, the book (company) side and the bank side. When the reconciliation is completed, both balances should match. What are we looking for?There are a number of items that can cause differences between your book and bank balances. Here is a list of the most common items you’ll encounter when doing a bank reconciliation:

How to startTo do a bank reconciliation, you’ll need a copy of the bank statement and a copy of all of the outstanding items in the checking account through the ending date of the bank statement. For some businesses, including my own, the bank statement does not close at the end of the month. Sometimes the statement end date is based on the date the account was opened. Once you have those two items, use a pencil or highlighter to mark off all the items that appear on both the bank statement and the check register. If an item appears on both, that means that the item was properly recorded and has cleared. After going through all the items, anything that remains unmarked is a an item that will need to be dealt with in the reconciliation. Create two columns on a piece of paper or use a spreadsheet to do the calculations for you. My bank reconciliations look like a large T-account. Start by writing the ending balance for the book and the bank under the appropriate column.  I like to do the bank side first because it is generally easier than the book side. You are only dealing with outstanding checks and deposits in transit on the bank side. List the deposits in transit and the outstanding checks. Add the deposits in transit to the beginning balance and subtract the outstanding checks. The bank side is relatively easy to do. That is why I like to do that side first. It is more likely to be correct if you have an error in your reconciliation. Most students who have errors have them on the book side. Being confident in the bank side helps resolve errors on the book side. On the book side, most items are fairly simple. Subtract bank service charges and add interest income. Subtract returned checks. Add unrecorded deposits and subtract unrecorded withdrawals. The last item, recording errors, requires a bit more thinking. Let’s imagine that you recorded a check for $715, but the bank cleared that check for $751. The check was used to pay for utilities and was recorded to utilities expense for $715. If the check cleared for $751, what happened to your utilities expense? Did it increase or decrease? It increased because more was paid for utilities. If the expense increased, cash must have decreased. Therefore, cash must be adjusted down or decreased by $36. This would be subtracted from book side of the reconciliation. Thinking about what is happening to your expenses can help you work your way through the problem. Once you have worked through all the remaining items on the book side, compute the reconciled balance for the books. When you are finished, the reconciled balances should agree. If they do not, take the difference between the two balances. Does that amount stick out in your mind. Check to see if there is a missing item for that amount that you might have forgotten to record. You may have forgotten multiple items. Place them in the reconciliation and see if you now balance. If you do not have an item for that amount, take the difference and divide it by 2. Look for that amount. If that amount appears in your reconciliation, you added (or subtracted) the amount when you should have subtracted (or added) the amount. Reverse the sign and check your balance again. Once you finish the bank reconciliation, there is one more step in the process. All the items that you recorded on the book side of the reconciliation must be recorded in the company’s accounting system. Prepare a journal entry (or several) to record those items. I usually record one large journal entry but you can also record a separate entry for each item in the reconciliation. Only record items on the book side! Bank reconciliations become easier as you do more of them. Get all the practice you can. Here is the bank reconciliation problem I created for the video on this subject. You are provided with the check register and the bank statement. See if you can complete the reconciliation before watching the video. Related Videos:How to do a bank reconciliation Journal entries for the bank reconciliation What would cause the balance of cash in the bank statement not to equal the balance of cash in the accounting records?Which of the following items would cause the balance of cash in the bank statement not to equal the balance of cash in the accounting records? Cash receipts by the company that have not been deposited in the bank.

What is the possible reason if the balance shown on an entity's bank statement less than the correct cash balance and neither the entity nor the bank has any errors?Error, fraud, and timing issues are all reasons that the cash balance per the bank statement and the cash balance per the books may vary. This creates the need for a bank reconciliation where a company accountant compares the two balances and accounts for any differences between the two.

Which of the following might be a reason when a bank statement shows greater balance then the cash book balance?Cheque issued by the bank but not yet presented for payment is one reason for bank pass book showing higher balance than cash book. When cheques are issued by the firm to suppliers or creditors of the firm, these are immediately entered on the credit side of the cash book.

What are the reasons for the differences between the balance of the bank statement and the bank column of the cash book?The reasons for the difference between the balance on the bank statement and the balance on the books consist of;. Outstanding checks.. Deposits in transit.. Bank service charges.. Check printing charges.. Errors in the books.. Errors by the bank.. Electronic charges on the bank statement are not yet recorded in the books.. |